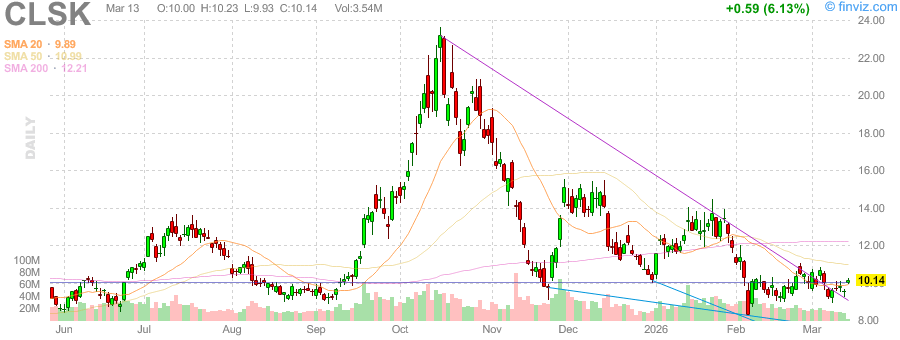

Bitcoin hit $73,000 this morning. CleanSpark — the largest pure-play Bitcoin miner on the NASDAQ — is up 5.76% on the day at $10.10. It’s also still 57% below its 52-week high of $23.61, despite holding 13,363 Bitcoin worth roughly $976 million. That treasury alone is 38% of the company’s entire market cap.

Meanwhile, 34.49% of the float is short. Twelve analysts rate it a Strong Buy with an average price target of $19.69.

This is either a coiled spring or a value trap. Here’s what the data actually shows.

What They Run

CleanSpark (Nasdaq: CLSK) operates large-scale Bitcoin mining data centers across Georgia, Tennessee, and an expanding Texas portfolio. They run 235,588 ASIC miners with a peak operational hashrate of 50.0 exahashes per second (EH/s) — the highest among major publicly traded pure-play Bitcoin miners. MARA Holdings runs roughly 36 EH/s; Riot Platforms is around 20 EH/s.

The Georgia and Tennessee sites have legacy power agreements locked in at $0.03–$0.04/kWh. They hold 1.8 GW of contracted power capacity total, with 808 MW currently utilized. The February 2026 operational update closed a second Texas campus, adding 300 MW of ERCOT-approved capacity to the portfolio.

In February, CleanSpark mined 568 Bitcoin and sold 553 of them for $36.65M — an average sale price of $66,266 per coin. At today’s $73,000 spot price, the same production would generate $41.5M. Year-to-date through February: 1,141 BTC mined.

The Financials: One Really Good Year, Then an Accounting Mess

CleanSpark’s fiscal year ends September 30. FY2025 looked like this:

- Revenue: $766.3M (+102% year-over-year, up from $379M in FY2024)

- Net income: $353.3M

- EBITDA margin: 87%

- Gross margin: 55.2%

- Operating margin: 41.6%

Revenue doubled for the second consecutive year. The company was legitimately profitable on an annual basis.

Then Q1 FY2026 (October–December 2025) filed. Revenue came in at $181.2M (+11.6% YoY) — but net loss hit $378.7M. The culprit: ASC 820 fair value accounting forces unrealized changes in Bitcoin holdings directly onto the income statement. When BTC pulled back from its late 2024 peak through the quarter, CLSK had to mark down its $1B+ treasury, generating a non-cash paper loss that dwarfed operating income.

What’s harder to explain away: adjusted EBITDA for Q1 was $(295.4)M. That’s not just accounting noise — it means the expansion buildout is consuming cash aggressively.

Balance sheet at December 31, 2025:

- Cash and equivalents: $458.1M

- Bitcoin holdings: $1.0B (at Dec prices; worth ~$976M at today’s $73K)

- Total assets: $3.3B

- Long-term debt: $1.8B

- Working capital: $1.3B

The debt is significant. CleanSpark issued zero-coupon Convertible Senior Notes due 2032 and uses bitcoin-backed lending facilities. Combined with continuous share issuance — shares outstanding grew 23.68% year-over-year — the capital structure requires Bitcoin to cooperate.

The Treasury Math

At $10.10/share with 255.75M shares outstanding, CleanSpark’s market cap is $2.58B.

Break it down: Bitcoin holdings at $73K = $975.5M. Cash = $458.1M. BTC + cash alone = $1.43B. You’re paying ~$1.15B for the operating infrastructure: 50 EH/s of mining capacity, 1.8 GW of contracted power, 235,588+ miners, and Texas land positions spanning hundreds of acres. Building that from scratch today would cost well over $1.5B.

Each $10,000 move in Bitcoin changes the treasury value by ~$133.6M. At $80K BTC, the treasury alone would be worth $1.07B — more than 41% of market cap at current prices.

Texas: The Bet on What Comes Next

The most important strategic development isn’t the mining rate — it’s what CleanSpark is buying in Texas.

The Brazoria County acquisition (447 acres near Houston, expected to close Q1 2026) provides 300 MW of initial power with optionality to expand to 600 MW, using transmission-level grid access. The second Texas campus (closed February 2026, 300 MW ERCOT-approved) brings total Texas contracted capacity approaching 1 GW when fully developed.

CleanSpark has been explicit: these Texas sites are designed to support AI and high-performance computing workloads alongside Bitcoin mining. Sub-$0.04/kWh transmission-level power in Texas is genuinely scarce. If CLSK converts even 20% of that capacity to HPC hosting, the revenue-per-watt jumps dramatically — AI data center hosting generates $300–$500K per megawatt per year in revenue, independent of Bitcoin price.

The specific risk: ERCOT’s batch study process for the Sealy project has faced timeline uncertainty, per Keefe Bruyette’s February analysis. Multiple Texas sites reduce single-project dependence, but ERCOT delays are a real execution risk.

Bull Case

1. The treasury makes the valuation math work. With Bitcoin above $70K, BTC + cash = $1.43B on a $2.58B market cap. You’re getting the entire mining infrastructure at ~$1.15B — below what it would cost to build.

2. Revenue trajectory is hard to ignore. $168M → $379M → $766M over three consecutive fiscal years. At 40% growth, FY2026 revenue tops $1.07B.

3. Short squeeze math is dangerous for bears. 34.49% short float, 3.24 days to cover. The Tradr 2x short ETF (CLSZ) launched February 19, amplifying short exposure. If Bitcoin clears $80K with conviction, margin call pressure becomes self-reinforcing.

4. JP Morgan went overweight in November. JPM upgraded CLSK from neutral → overweight citing the low-cost power position as structurally undervalued given post-halving mining economics. Nobody has a sell rating. Skeptics are expressing their view through short positions, not analyst downgrades.

5. AI optionality in Texas is real capital. They’re not talking about pivoting to AI — they’re buying land specifically positioned for it. If the HPC pivot lands even partially, the revenue model and the multiple both change.

Bear Case

1. $1.8B in debt cuts both ways. At $40K BTC, the treasury drops to $534M, working capital tightens, and the debt overhang becomes the story. The zero-coupon converts due 2032 look manageable until they don’t.

2. Dilution is structural. 23.68% YoY share count growth. They fund expansion through equity markets. There’s no obvious end to this cycle until the company becomes self-funding from mining cash flows — which requires sustained BTC above $65K or so.

3. Q1 operating losses aren’t all accounting. Adjusted EBITDA of $(295.4)M for Q1 FY2026. Expansion capex, costs from new sites coming online, and debt service are compressing near-term cash generation. Actual profitability is a 2026–2027 story.

Analyst Targets

Twelve analysts cover CLSK with a Strong Buy consensus and an average 12-month price target of $19.69 — 93% above the current $10.10.

- JP Morgan: Overweight (upgraded November 2025)

- Needham: Buy, $25 target (raised November 2025)

- Northland Capital: Outperform, $22.50 (initiated January 13, 2026)

- Maxim Group: Buy, $22 (initiated January 8, 2026)

- B. Riley Securities: Buy, $16 (initiated July 2025)

The bull/bear split runs entirely through the short book. Sophisticated bears are betting on timing and leverage risk — not disagreeing with the asset valuation.

Verdict

CleanSpark is a leveraged bet on Bitcoin. That’s a description, not a criticism.

At $10.10, the stock prices in real uncertainty: BTC volatility risk, $1.8B in debt, ongoing dilution, and ERCOT execution on Texas. The 34% short interest tells you sophisticated money sees genuine downside scenarios.

The counter: 93% analyst upside consensus, $976M in BTC on the balance sheet, $458M in cash, and 50 EH/s of mining capacity scaling toward 1 GW+ in Texas. At Bitcoin above $70K, the asset base is difficult to argue with at current prices.

Compelling at $10–12 with Bitcoin above $70K. If BTC breaks $80K, short squeeze pressure could close a meaningful chunk of the gap to the $19.69 analyst target in a hurry. Watch Q2 FY2026 earnings (expected May 2026) for Texas capacity timelines and whether operating costs are trending down as new sites stabilize.

If Bitcoin drops back below $55K, revisit the thesis. The leverage cuts both ways.

This is not financial advice. I hold no position in CLSK. Do your own research.

Related: Exodus Movement (EXOD): The Crypto Wallet Company Trading at a P/E of 4 | SEC EDGAR 8-K Filings: Spot Small-Cap Moves Before the Crowd | AMPL Up 17.87% in 11 Days: Our Ampleforth Position Update