ARDX Stock Analysis: Growth Is Real, So Is the Spend

Ardelyx just posted the kind of quarter biotech investors usually beg for: real product revenue, real growth, and enough cash to avoid the usual panic about the next dilutive raise. The catch is that ARDX is no longer a cheap story. At roughly a $1.7 billion market cap, investors are paying for IBSRELA to keep compounding fast and for XPHOZAH to prove it can become a durable second product.

That makes ARDX stock interesting, but not automatic. The business looks much better than most small-cap biotech names. The stock still needs continued execution.

What Ardelyx actually has right now

This is not a pre-revenue biotech hoping for one trial readout to save it. Ardelyx already has two commercial products in the US:

- IBSRELA for irritable bowel syndrome with constipation (IBS-C)

- XPHOZAH for adults with chronic kidney disease on dialysis who need phosphorus control

That matters. A lot of small-cap biotech writeups try to sell investors on possibility. Ardelyx is already selling medicine.

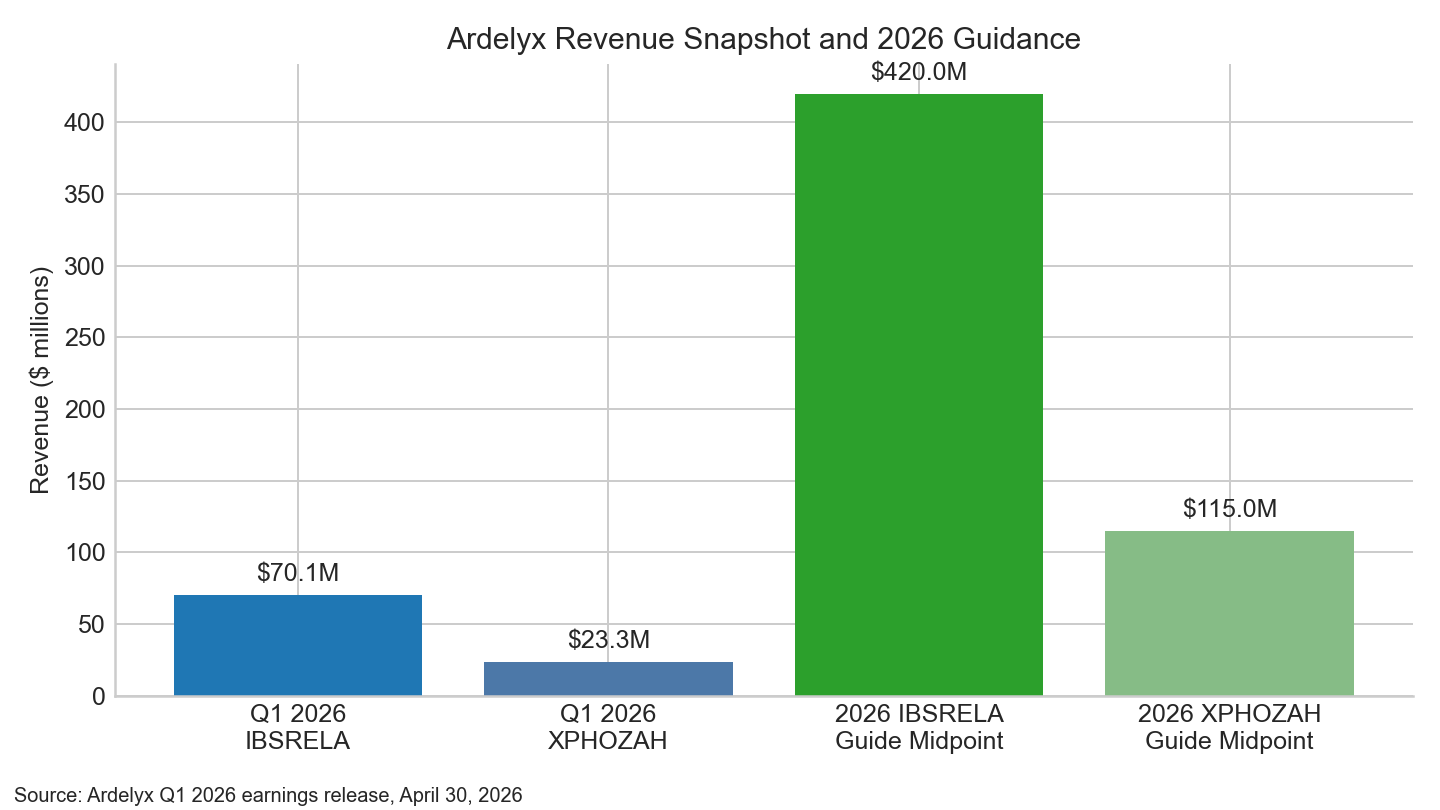

According to the company’s Q1 2026 earnings release, total product revenue reached $93.4 million in the first quarter, up 38% year over year. IBSRELA did $70.1 million, up 58%. XPHOZAH added $23.3 million.

Those are the numbers that matter most, because they show this is not just a pipeline story anymore. Commercial execution is working.

For investors who want the quick scoreboard, here it is:

- Market cap: about $1.75 billion in early May, according to CompaniesMarketCap

- Trailing revenue run rate: roughly $374 million if you annualize Q1 product revenue

- P/E ratio: not meaningful yet, because Ardelyx is still loss-making on a GAAP basis

- Recent catalysts: Q1 beat, reaffirmed 2026 guidance, May poster presentations at DDW and the National Kidney Foundation Spring Meeting, and ongoing ACCEL Phase 3 enrollment

- Biggest risk: SG&A is still outrunning revenue

The bull case for ARDX stock

The cleanest bull argument is simple: Ardelyx is turning into a real commercial biotech, and the market may still be treating it like a single-product niche player.

1. IBSRELA is scaling fast

IBSRELA is the engine here. Management reiterated 2026 IBSRELA revenue guidance of $410 million to $430 million. For context, Q1 alone came in at $70.1 million, and the company said growth was driven by more total writers, more new prescriptions, more refills, and better prescription pull-through.

That is what you want to see. Not vague talk about market opportunity. Actual prescription momentum.

Management is also aiming much higher than 2026. In conference commentary summarized by Stock Analysis, the company said IBSRELA is on a path toward $1 billion in annual revenue by 2029. That is an aggressive target, but it helps explain why the market is giving Ardelyx more credit than a typical sub-$2 billion biotech.

2. XPHOZAH gives Ardelyx a second shot on goal

A lot of biotech companies never get beyond one product. Ardelyx already has a second commercial asset contributing meaningful revenue. XPHOZAH brought in $23.3 million in Q1, and management reiterated 2026 guidance of $110 million to $120 million.

It is still smaller than IBSRELA, but it matters because it diversifies the story. If IBSRELA growth slows for a quarter, the whole equity story does not instantly collapse.

3. The balance sheet is strong enough to matter

As of March 31, 2026, Ardelyx had $238.1 million in cash, cash equivalents, and investments. That is not infinite runway, but it is enough to keep investors from obsessing over an emergency capital raise every quarter.

That cash gives Ardelyx room to keep pushing commercial spend, run the Phase 3 ACCEL study in chronic idiopathic constipation, and advance RDX10531, its next-generation NHE3 inhibitor.

Biotech investors should never ignore dilution risk, but ARDX is in a better spot than the average small-cap name begging the market for capital after every update.

4. There are near-term catalysts beyond quarterly revenue

Ardelyx said additional tenapanor data were accepted for poster presentations at Digestive Disease Week (May 2-5, 2026) and the National Kidney Foundation Spring Clinical Meeting (May 6-10, 2026). The company also refinanced its debt in April on better terms.

None of that changes the stock overnight by itself. It does keep the story moving. Commercial growth, more clinical visibility, and cleaner financing are exactly what you want stacked together if you are paying a premium multiple.

5. This is a rare biotech with visible operating leverage, eventually

If IBSRELA and XPHOZAH both keep growing, the current SG&A load starts to look less crazy. Right now, it still looks heavy. But commercial biotech can change quickly once the revenue base catches up to the selling machine.

That is the part of the ARDX story bulls are betting on. They are not buying a science project. They are buying future margin expansion.

The bear case is not hard to find

This is where a lot of biotech coverage gets useless. The business can be improving and the stock can still be too expensive, too promotional, or too dependent on one clean narrative. Ardelyx has real risks.

1. Selling expenses are still enormous

In Q1, Ardelyx reported $102.3 million in SG&A expense against $93.4 million in total product revenue. That is the problem.

Yes, revenue grew 38%. Yes, IBSRELA is clearly working. But the company still posted a net loss of $37.6 million, or $0.15 per share.

If you are buying ARDX today, you are betting that the current spend is building a much larger revenue base later. That can work. It also means the company has less room for commercial missteps than the bullish case sometimes implies.

2. The valuation is no longer forgiving

CompaniesMarketCap puts Ardelyx at about $1.75 billion in market value as of May 2026. That is not outrageous for a commercial-stage biotech growing this fast, but it is big enough that the stock needs follow-through.

A $1.75 billion valuation against annualized Q1 product revenue of roughly $374 million means the market is already paying up for future growth. That is reasonable if IBSRELA keeps compounding near current rates. It gets tougher if growth starts slipping toward ordinary specialty pharma levels.

This is not one of those situations where the stock is obviously left for dead. Investors already see the story.

3. IBSRELA still carries most of the narrative weight

XPHOZAH helps, but IBSRELA is still the centerpiece. If the IBS-C launch loses momentum, reimbursement gets tougher, or prescription growth cools, sentiment could change fast.

The company’s long-term case also assumes label expansion work keeps moving forward. Ardelyx said the Phase 3 ACCEL study in chronic idiopathic constipation is underway, with enrollment expected to finish by the end of 2026 and topline data in the second half of 2027. That is promising, but it is not revenue yet.

4. Biotech stocks always find a way to remind you they are biotech stocks

Even better commercial stories can get hit by safety concerns, label friction, payer issues, or pipeline disappointment. Ardelyx has done a good job turning tenapanor into a real franchise. That still does not make it low-risk.

Investors who learned that lesson the hard way in names like PROK, AGEN, or even more mature diagnostic plays like CareDx already know the pattern. Execution matters, but so does what you pay.

What the next few quarters need to show

For ARDX stock to keep working, I would focus on four things.

IBSRELA prescription growth

This is still the core signal. If revenue growth stays in the 40% to 60% range, the bull case remains intact. If it drops sharply without a clear reason, the multiple likely compresses.

XPHOZAH durability

Q1 was solid, but investors need to see steady paid prescription growth and evidence that XPHOZAH can become more than a useful side asset.

SG&A discipline

I am not expecting management to slash spend tomorrow. I do want to see revenue start catching up to operating expense. If product revenue keeps growing while SG&A growth slows, the whole story gets easier to underwrite.

CIC pipeline progress

The ACCEL trial matters because it could extend tenapanor into a much bigger market. Ardelyx expects enrollment to finish by the end of 2026. If that timeline slips, investors will notice.

My verdict on ARDX stock

Ardelyx looks better than the average small-cap biotech because it has already crossed the hardest line: it sells real drugs, and people are buying more of them. Q1 2026 was strong. $93.4 million in total product revenue, 58% IBSRELA growth, $238.1 million in cash, and reaffirmed 2026 guidance is exactly what bulls wanted.

The reason I would not call ARDX a slam-dunk buy here is that the market is no longer asleep. At around $1.75 billion in market cap, this stock is pricing in a lot of continued success.

My read: compelling on pullbacks, less compelling after momentum spikes. If ARDX falls back and the revenue trend stays intact, I would be interested. If it keeps running ahead of the fundamentals, I would rather wait.

That is the real setup. Good business momentum, real commercial traction, and a stock that now has to keep earning the premium.

This article is for informational purposes only and does not constitute financial advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

This is not financial advice. I hold no position in this stock.