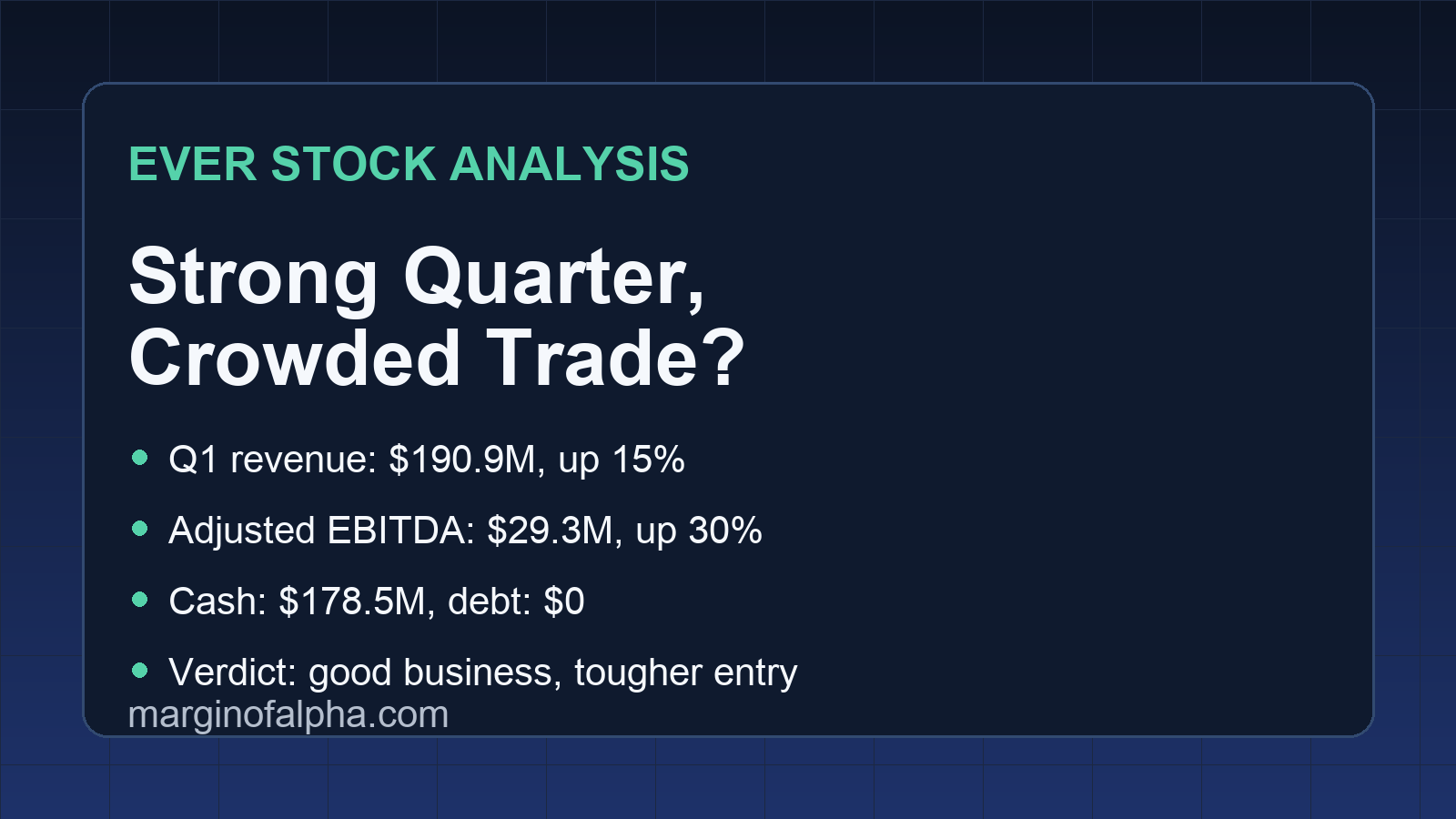

EverQuote just printed another strong quarter, and the business is cleaner than most small-cap internet names. Q1 2026 revenue grew 15% year over year to $190.9 million, adjusted EBITDA rose 30% to a record $29.3 million, and the company ended the quarter with $178.5 million in cash and no debt. For a stock with a market cap around $660 million, that matters.

The problem is simpler: the easy money may already be gone. Shares ripped after earnings, and this is no longer the same setup as a sleepy ignored small cap at 10x earnings with no audience. EverQuote still looks like a legitimate paper-portfolio name, but at current levels the thesis has shifted from “nobody sees it” to “can execution stay hot enough to justify the rerating?”

The target keyword: EVER stock analysis

If you searched for an EVER stock analysis because the stock suddenly showed up on your screen after earnings, the headline number is this: EverQuote is executing well, but you are now paying for that execution.

This is not a broken turnaround story anymore. It is a profitable digital insurance marketplace with real cash flow, a buyback, no debt, and management openly aiming for $1 billion in annual revenue within 2 to 3 years. That is the bull case. The bear case is that insurance ad budgets are cyclical, variable marketing spend is rising with volume, and a stock that just got discovered can still punish late buyers.

What EverQuote actually does

EverQuote runs a marketplace that helps carriers and local agents buy customer acquisition across digital channels. In plain English, it helps insurance companies find people shopping for auto, home, and renters coverage.

That business model can be ugly when traffic costs spike or insurance carriers pull back. It can also be very lucrative when underwriting conditions improve and carriers want growth. Right now, EverQuote is clearly in the good part of that cycle.

Q1 2026 numbers were strong across the board:

- Revenue: $190.9 million, up 15% year over year

- Auto insurance revenue: $172.4 million, up 13%

- Home and renters revenue: $18.5 million, up 33%

- GAAP net income: $18.7 million, versus $8.0 million a year ago

- Adjusted EBITDA: $29.3 million, up 30%

- Operating cash flow: $29.6 million

- Cash: $178.5 million

- Debt: zero

- Share repurchases in Q1: 1.1 million shares for about $19.9 million

Those are not “adjusted story stock” numbers. Those are real operating results.

Why the market suddenly cares

There are three reasons EverQuote has become more interesting.

First, carrier demand looks healthy. Management said the quarter benefited from a growth-oriented carrier environment, and one top-five carrier more than doubled its expected spend in the back half of the quarter. That matters because EverQuote’s marketplace works best when big insurance buyers want to press on customer acquisition.

Second, the company is showing real margin improvement. Revenue rose 15%, but adjusted EBITDA rose 30% and operating cash flow hit a record. Management also said operating expenses have stayed nearly flat over two years despite revenue roughly doubling. That is exactly what you want to see from a marketplace business whose software and automation stack can scale.

Third, management is wrapping the next leg of the story in AI. Usually that is where I roll my eyes. Here, it is at least tied to something specific. EverQuote says smart campaigns, AI-powered bidding, and internal agentic AI tools are already helping drive customer value and internal productivity. On the Q1 call, management said smart campaigns are now being extended to local agents for the first time, not just carriers. They also said they are preparing for LLM-originated traffic and technical integrations with AI search platforms.

You should still be skeptical of any management team saying “AI” on an earnings call in 2026. But in EverQuote’s case, the business is already profitable before any blue-sky AI upside. That makes the AI angle additive, not the entire thesis.

The bull case for EVER

The bull case starts with quality. EverQuote is not burning cash to chase hypothetical scale. It is already profitable, already producing strong operating cash flow, and already buying back stock.

At roughly a $660 million market cap, the balance sheet matters a lot. With $178.5 million in cash and no debt, a big chunk of the enterprise value is covered by cash. That gives management flexibility to keep buying back shares, invest in product, or simply ride out a softer insurance cycle better than weaker peers.

There is also a straightforward growth case. Management guided for Q2 2026 revenue of $185 million to $195 million, which implies 21% year over year growth at the midpoint. That is actually faster than the 15% growth posted in Q1. They also guided for adjusted EBITDA of $28 million to $30 million, up 32% at the midpoint.

If EverQuote can keep putting up mid-teens to low-20s revenue growth while expanding EBITDA and cash flow, the market will keep rerating it. Small caps with real profits and clean balance sheets do not stay ignored forever.

I also like that the growth is not purely coming from one tiny experiment. Auto revenue remains the core at $172.4 million, while home and renters grew 33% to $18.5 million. That second leg is still smaller, but it shows the company is not boxed into one product line forever.

Finally, the path to $1 billion in annual revenue is aggressive but not absurd. EverQuote did about $191 million in Q1 alone. Annualize that and you are already above a $760 million run rate. If the company can sustain low- to mid-teen growth plus some share gains, $1 billion in 2 to 3 years is plausible.

The bear case for EVER

This is where you should slow down.

The biggest risk is that EverQuote is still tied to insurance advertising demand. If carrier budgets tighten, underwriting conditions worsen, or acquisition appetite cools, EverQuote feels it. This is not a subscription software business with locked-in recurring revenue. It is a marketplace. Good cycles feel great. Bad cycles can get ugly fast.

Variable Marketing Dollars also rose to $55.9 million from $46.9 million. That is not automatically bad, since the company is scaling volume, but it is a reminder that traffic acquisition is not free and margins can get pressured if unit economics move the wrong way.

The second risk is valuation discipline. This article is going up after the company already reported a huge quarter and grabbed attention. A stock can be a much better business and a much worse trade after a sharp move. If you are buying now, you are betting the next few quarters stay clean enough to support the new price level.

Third, the AI angle can become a trap if investors get carried away. Smart campaigns and LLM traffic integrations are interesting, but they are not proven giant revenue buckets yet. If the market starts valuing EverQuote like a pure-play AI platform instead of a cyclical, execution-driven insurance marketplace, expectations can outrun fundamentals.

There is also concentration risk in large carrier spending. When management says one top-five carrier more than doubled expected spend late in the quarter, that is good news for the quarter. It is also a reminder that large customers matter a lot.

My view on valuation and position sizing

I think EverQuote belongs on the paper portfolio because the fundamentals are real. This is not a concept stock pretending to be a business. It has earnings, cash flow, cash on the balance sheet, no debt, and a management team that is at least talking about growth from a position of strength.

But I would not treat it like a table-pounding deep-value setup after the post-earnings move.

The better framing is this: EVER is now a quality small-cap momentum name with fundamental support. That can still work. It just means your entry matters more.

If the stock pulls back and the underlying numbers stay intact, I would be much more interested. Chasing vertical moves in small caps is how you turn a good thesis into a bad trade.

That is also why the portfolio position here should stay disciplined. A stock with this kind of setup can absolutely keep running. It can also round-trip 20% to 30% if the next quarter is merely good instead of spectacular.

How EVER compares with other marginofalpha setups

Compared with some of the biotech names we have covered, EverQuote is less binary. There is no Phase 2 data readout deciding everything overnight. Compared with earlier deep-value software names, it has better current profitability. Compared with some industrial catalyst stories, it has less balance-sheet risk.

That is the appeal.

The tradeoff is that EverQuote probably has less “nobody understands this” upside than a truly underfollowed oddball small cap. The market understands insurance lead generation. If EverQuote keeps compounding, the stock can work well. If growth cools, it probably derates just as quickly as it rerated.

That is why this is a good analysis name right now. It sits in the middle ground between quality and cyclicality, which is where a lot of investors get lazy.

Final verdict on EVER stock

My EVER stock analysis is pretty simple: the business is better than most small-cap internet names, but the stock is less compelling after the post-earnings surge.

If you already own it from lower levels, holding still makes sense. If you are new, I would start small and wait for a calmer entry instead of buying someone else’s excitement.

EverQuote is one of the cleaner small-cap internet stories on the board right now. I like the business. I just do not love the setup after the crowd noticed it.

For more small-cap breakdowns, read our HYLN stock analysis, our CPRX stock analysis, and our safe withdrawal rate guide.

This article is for informational purposes only and does not constitute financial advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.