PBYI Stock Analysis: Puma Biotechnology Looks Cheap, but the Pipeline Still Has to Matter

This PBYI stock analysis starts with the obvious part: Puma Biotechnology looks cheap on a screen. The company is profitable, it trades around 12x trailing earnings, it finished 2025 with $97.5 million in cash and marketable securities, and management is guiding to another profitable year in 2026. At roughly a $381 million market cap, that is cheap enough to get attention.

The problem is that Puma is still mostly a one-drug story.

NERLYNX keeps the lights on. The real debate is whether investors should pay up for the alisertib pipeline on top of that base business, or treat Puma as a mature oncology commercial asset with limited growth. That tension is exactly why the stock still looks stuck.

My take is simple: PBYI is interesting because it is cheap, cash-generative, and has near-term clinical catalysts. But it is not a slam dunk. If alisertib disappoints, this probably stays a low-multiple biotech value trap instead of re-rating higher.

The setup: profitable biotech, low expectations

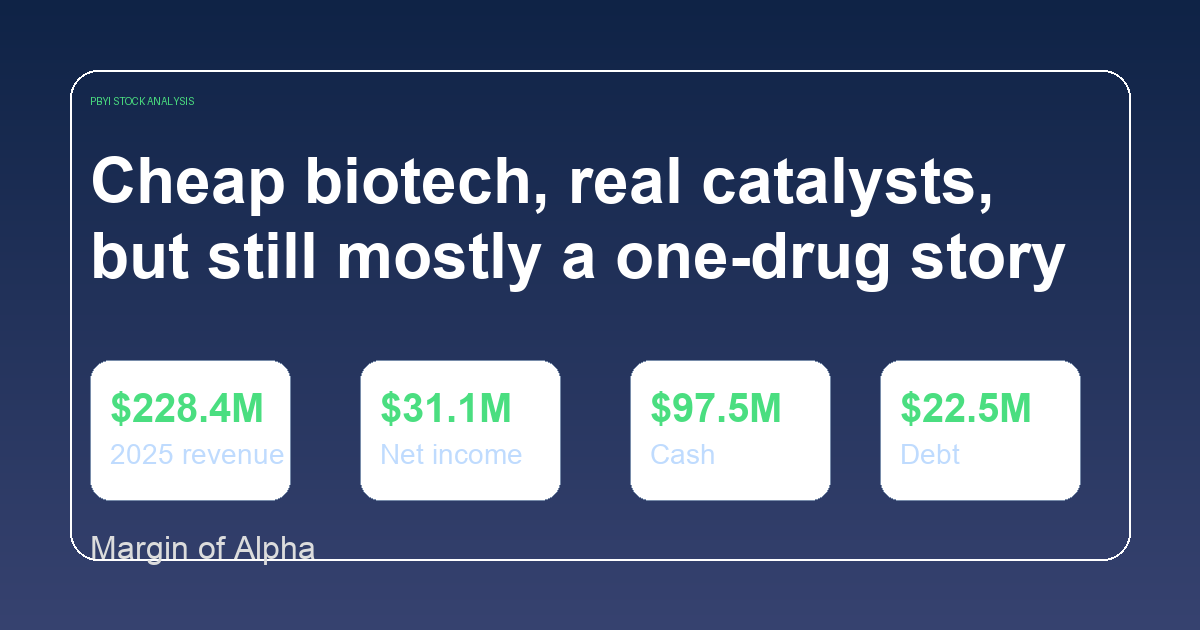

Puma reported full-year 2025 revenue of $228.4 million. Of that total, $204.1 million came from NERLYNX product revenue and $24.3 million came from royalty revenue. Full-year GAAP net income was $31.1 million, or $0.61 diluted EPS. Non-GAAP adjusted net income was $38.1 million, or $0.75 diluted EPS. You can see the company’s full release on Puma’s investor news page.

Those are not fake numbers dressed up by endless adjustments. Puma has now posted three consecutive profitable years, which matters in a sector full of cash-burning stories that are constantly one secondary offering away from trouble.

A few numbers stand out:

- Market cap: about $381 million

- Share price: about $7.49

- Cash per share: $1.96

- Total debt: $22.5 million at year-end 2025

- Trailing P/E: 12.26x

- Forward P/E: 14.98x

- Analyst target price: $5.00 on Finviz data

- Short float: 10.8%

That is a strange profile. Usually, a profitable oncology company with a commercial drug, net income, and nearly $100 million in liquidity does not look this discounted unless the market has serious doubts about future growth.

The market's skepticism is not hard to understand.

NERLYNX is steady, but it is not a hypergrowth story

In the fourth quarter of 2025, Puma generated $75.5 million in total revenue, up from $59.1 million a year earlier. Product revenue was $59.9 million versus $54.4 million in the prior-year quarter. That part looks solid.

But the full-year picture is less exciting. Total 2025 revenue of $228.4 million was actually slightly below the $230.5 million posted in 2024. Product revenue improved, but royalty revenue fell from $35.3 million to $24.3 million.

That explains why Puma still trades like a business in runoff instead of a growth stock. NERLYNX is durable, but it is not enough by itself to create a big new multiple.

Management's 2026 guide reinforces that point:

- Net NERLYNX product revenue: $194 million to $198 million

- Royalty revenue: $20 million to $23 million

- Full-year net income: $10 million to $13 million

- Q1 2026 net product revenue: $36 million to $39 million

- Q1 2026 royalty revenue: $2 million to $3 million

That is still a profitable business. It just is not a business with obvious top-line acceleration.

If you buy PBYI today, you are not buying a clean growth story. You are buying a stable oncology commercial franchise plus a call option on alisertib.

Why the pipeline matters more than the income statement

The bull case depends on alisertib.

Puma licensed alisertib in 2022 and is now pushing it through two Phase II programs:

- ALISCA-Breast1 in HER2-negative, hormone receptor-positive metastatic breast cancer

- ALISCA-Lung1 in extensive-stage small cell lung cancer

Management laid out three meaningful milestones over the next 12 months:

- Interim ALISCA-Breast1 data in Q2 2026

- Additional ALISCA-Lung1 interim data in Q2 2026

- Updated ALISCA-Breast1 data in Q4 2026

That is the real reason to care about Puma in 2026.

If those readouts are encouraging, the market can stop valuing Puma as a sleepy one-product biotech and start valuing it as a profitable oncology platform with a second act. If the data are mediocre, the stock probably stays cheap for a reason.

This is what makes PBYI more interesting than a typical value screen biotech. There is an actual catalyst calendar here, not just vague hope.

Why the valuation looks cheap anyway

At roughly $381 million in market value, Puma is trading at about 1.7x 2025 revenue and around 12x trailing earnings. For biotech, that is low. Even plenty of mediocre specialty pharma names trade at richer multiples than that when they have steady cash flow and some pipeline optionality.

The balance sheet helps too. Puma ended 2025 with $97.5 million in cash, cash equivalents, and marketable securities, against only $22.5 million of total debt. That is not a fortress balance sheet by mega-cap standards, but for a small-cap biotech it is clean enough to matter.

The company also generated $41.8 million in operating cash flow in 2025. That is a real number I care about more than most adjusted biotech metrics.

If you strip out some of the balance sheet value, the enterprise value is even smaller than the market cap suggests. That means investors are paying a pretty modest price for the commercial business and getting the alisertib readouts at a discount.

That is the heart of the bull case.

The bull case for PBYI

Here is why the stock can work from here.

First, Puma is already profitable. This is not a lottery-ticket biotech with no approved products and no financial discipline. The core NERLYNX business throws off cash.

Second, management has reduced debt meaningfully, from $67.0 million at the end of 2024 to $22.5 million at the end of 2025. That lowers financial risk and gives Puma more flexibility if trial spending rises.

Third, 2026 should bring multiple clinical catalysts, especially the Q2 alisertib updates. Small-cap biotech names do not need perfect data to move. They need data that keeps the story alive and raises the ceiling.

Fourth, short interest is high enough at 10.8% of float to matter if the company posts strong Q1 results on May 7 or if interim trial data beat expectations.

Finally, the valuation is already skeptical. This stock does not need a heroic assumption to work. If Puma can simply prove that alisertib has a real shot and keep NERLYNX stable, the multiple can expand from here.

The bear case is very real

I would not describe PBYI as a safe biotech value play.

The biggest risk is concentration. Puma still depends heavily on NERLYNX. That creates a ceiling on how much confidence investors will give the stock until a second asset becomes more credible.

The second risk is pipeline execution. Phase II data can revive a story or bury it. If alisertib disappoints in either breast cancer or small cell lung cancer, the market may decide Puma is just an ex-growth commercial oncology company. Those businesses rarely get exciting multiples.

Third, 2026 guidance already tells you profitability is expected to decline. Management guided to $10 million to $13 million in full-year net income, down from $31.1 million in 2025. Some of that reflects pipeline investment, but it still matters. Cheap stocks can get cheaper when earnings are moving the wrong way.

Fourth, royalty revenue is volatile. In 2025, total revenue looked flatter than product revenue because royalties dropped sharply from the prior year. That makes the overall story lumpier than the headline P/E ratio suggests.

Finally, analysts do not seem especially excited. Finviz currently shows a $5.00 target price, below the current share price, and Puma’s own May 7 Q1 conference call probably matters more than consensus targets right now. If you want to track the next catalyst directly, the company has already posted the Q1 2026 earnings call notice.

How I would frame the stock today

PBYI is not the kind of biotech I would buy just because it screens cheap.

I would buy it only if I wanted a small-cap healthcare name with three traits:

- a real commercial product,

- a still-profitable base business,

- and near-term pipeline readouts that could change the narrative.

That is a much narrower setup than a broad value pitch, but it is also more interesting.

Compared with higher-multiple healthcare names, Puma at least gives you some downside support from an existing drug franchise. Compared with pure pipeline names, it gives you actual earnings and cash flow. That middle ground is what makes it investable.

If you want other healthcare names on the site with cleaner growth stories, see our breakdown of ANI Pharmaceuticals, our take on CareDx after its big spike, and our look at AbCellera as a cash-rich biotech bet.

Verdict: cheap enough to watch, but the data need to hit

Puma Biotechnology is cheap for a reason, but that does not mean the market is right.

At about $381 million in market cap, with $228.4 million in 2025 revenue, $31.1 million in net income, $97.5 million in liquidity, and only $22.5 million in debt, PBYI is clearly not priced like a thriving growth biotech. It is priced like a company with one aging commercial asset and an uncertain pipeline.

That is fair, up to a point.

What makes the stock interesting here is that the bar is low. Puma does not need to become the next biotech darling. It just needs to keep NERLYNX stable and deliver alisertib data that investors can believe in.

If management does that, this stock can work. If not, it probably stays cheap and frustrating.

My view: PBYI is a reasonable speculative small-cap biotech watchlist name under $8, more compelling closer to $6.50 to $7.00, and much less attractive if the stock runs before the clinical data prove anything.

This article is for informational purposes only and does not constitute financial advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.