AbCellera looks cheap for a reason, but the setup is finally getting interesting. ABCL stock analysis in April 2026 comes down to three facts: revenue snapped back to $75.1 million in 2025, the company still has roughly $700 million of available liquidity, and lead menopause program ABCL635 has a real catalyst window with Phase 1 data due on the May 11 earnings call and Phase 2 results expected in Q3 2026.

The market is still treating AbCellera like a busted pandemic-era biotech tools name. That is fair if you only look at the income statement. It gets less fair when you notice the enterprise value is about $795 million against a company that finished 2025 with $533.8 million in cash, another $143.2 million in debt, a new clinical manufacturing facility, and two internal programs already in the clinic. This is no longer just a platform story. It is slowly becoming a pipeline story.

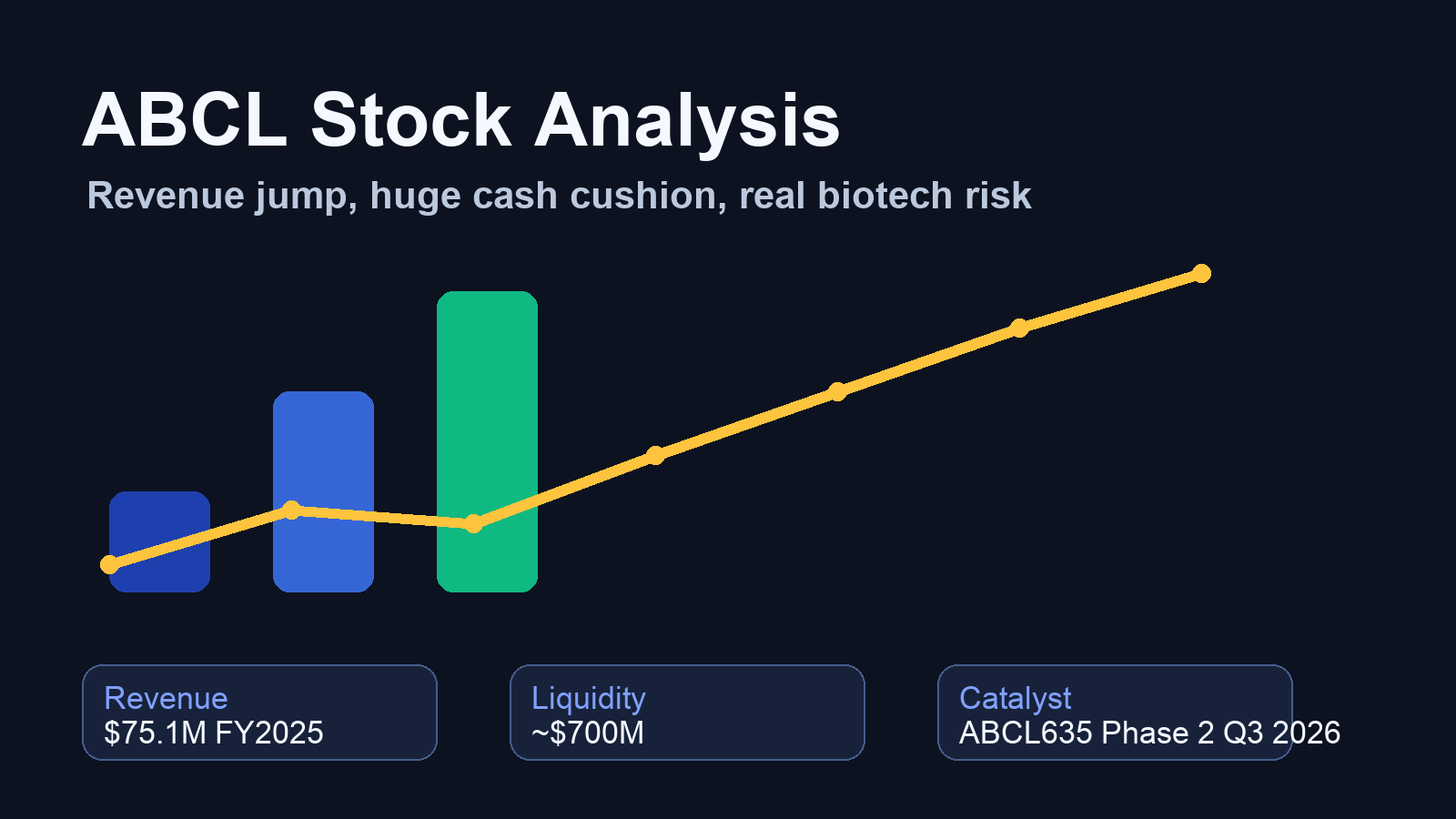

ABCL stock analysis starts with the balance sheet

If you buy ABCL today, you are not buying current earnings. You are buying time, optionality, and one potentially meaningful women’s health catalyst.

Here are the key numbers investors should care about:

- Market cap: about $1.17 billion

- Enterprise value: about $794.8 million

- FY2025 revenue: $75.1 million, up 160.6% year over year

- Net loss: $146.4 million, improved from $162.9 million in 2024

- Cash and equivalents: $533.8 million

- Total debt: $143.2 million

- Available liquidity: about $700 million, including government funding disclosed by the company

- Short interest: 50.4 million shares, or 24.4% of float

- Next earnings date: May 11, 2026

That balance sheet matters because AbCellera is still burning cash. Free cash flow was negative $174.1 million over the last 12 months. If the company were thinly capitalized, this would be a hard pass. It is not. Management has enough runway to push its internal pipeline forward without running to the market tomorrow morning.

That cash cushion is the main reason ABCL is worth watching instead of dismissing. A lot of clinical-stage biotech names trade like lottery tickets because they need a financing every time sentiment gets rough. AbCellera has more breathing room than that.

The real bull case is ABCL635, not the legacy platform story

The most important thing that changed over the last year is that ABCL635 stopped being a concept slide and became an actual clinical asset.

ABCL635 targets the neurokinin 3 receptor for moderate-to-severe vasomotor symptoms associated with menopause, basically hot flashes. That might sound less exciting than oncology, but the commercial logic is obvious. Menopause is a huge market, plenty of patients want a non-hormonal option, and management is clearly prioritizing this program.

The timeline matters here:

- ABCL635 entered the clinic in July 2025

- The company has already moved into the Phase 2 portion of the Phase 1/2 study after interim review of Phase 1 safety and target-engagement data

- AbCellera said it will disclose Phase 1 interim data on the May 11, 2026 earnings call

- Top-line Phase 2 results are expected in Q3 2026

That is the whole trade. If the Phase 1 update looks clean and Phase 2 efficacy has teeth, the market will start valuing AbCellera as a real clinical-stage biotech with a first-in-class women’s health asset. If the data disappoints, the stock probably drifts back toward cash-plus-platform value and stays dead money for a while.

There is a second internal program too. ABCL575 is in Phase 1 for atopic dermatitis and potentially broader inflammatory uses. That gives the story some depth, but right now ABCL635 is the one that can actually move the stock.

Why the 2025 revenue jump looks better than the headline skeptics think

On the surface, a 160.6% revenue jump to $75.1 million sounds like the turn is already here. I would not go that far. This is still a lumpy business. You are dealing with partner revenue, milestones, and a company transitioning from service platform to internal drug developer.

Still, the revenue rebound was not meaningless. AbCellera ended 2025 with 104 cumulative partner-initiated program starts and 19 molecules in the clinic. It also opened a clinical manufacturing facility, which matters because it gives the company more control over development and supply as its internal pipeline matures.

There was also a meaningful legal and economic win in late 2025. AbCellera settled global patent litigation with Bruker for $36 million up front plus future royalties tied to Beacon platform sales. That does not solve the valuation puzzle by itself, but it is another example of hidden asset value that the market is not giving full credit for.

This is why the name is more interesting than a basic screen suggests. If you just run a filter on negative earnings and negative free cash flow, ABCL fails. If you look underneath, you see a company with capital, an improving operating base, a maturing pipeline, and a catalyst schedule that is finally close enough for public investors to care.

The bear case is simple: cash burn plus biotech execution risk

You do not need to squint to find reasons this stock is still down in the single digits.

Start with the obvious one. AbCellera lost $146.4 million last year and burned $174.1 million of free cash flow. That is a real number, not some accounting quirk. If internal programs take longer than expected or partner economics stay weak, the company can keep destroying capital for years.

Second, gross margins were ugly because the current revenue base is too small against the company’s cost structure. This is what happens when a business was built for scale that has not arrived yet. The fixed-cost machine is there. The corresponding revenue still is not.

Third, biotech investors should not get cute about clinical risk. ABCL635 may be first-in-class, but first-in-class cuts both ways. You can get premium upside if the data are strong. You can also discover that the market opportunity or efficacy profile is less attractive than bulls hoped. Until we see Phase 2 data, this is still an informed speculation.

Fourth, short sellers are not gone. About 24.4% of float is sold short, with days to cover near 18.8. Bulls will look at that and dream about a squeeze. I look at it as a warning label. Plenty of sophisticated investors still think this story is overvalued, overbuilt, or too dependent on an unproven pipeline.

How ABCL stacks up against other recent marginofalpha setups

Compared with recent names we have covered, ABCL sits in a very different bucket. ANI Pharmaceuticals had a cleaner earnings-based value case. Remitly had visible profitability inflection. Phibro Animal Health had improving fundamentals but a richer multiple.

ABCL is messier than all three. It also has more binary upside if the pipeline works. That makes position sizing important. This is not the kind of stock I would want as a huge core holding before Q3 data. It is the kind of stock I understand owning as a smaller speculative position when the enterprise value is not much higher than the company’s net cash plus strategic assets.

ABCL valuation: compelling below $4, harder to love after a big pre-data spike

At about $3.86 per share, ABCL trades close to 1.2 times book value and about 15.8 times trailing sales. That sales multiple is not especially useful on its own because the current revenue base is still depressed and noisy.

The cleaner way to think about valuation is this:

- Enterprise value is under $800 million

- Liquidity is about $700 million

- The company has 19 molecules in clinic across partner programs

- ABCL635 has a near-term clinical readout path

- Analyst average price target sits around $8.40

I would not anchor blindly to the analyst target, but it tells you the same thing the chart does: expectations are still low. If the May update is clean and the Q3 readout is good, this stock does not need heroic assumptions to trade materially higher. If sentiment gets ahead of itself and the stock rips into the $6 to $7 range before Phase 2 data, the risk-reward gets worse fast because then you are paying up for data you still have not seen.

My verdict on ABCL stock in 2026

ABCL is one of the better speculative biotech setups on the site’s paper portfolio right now because the balance sheet buys management time and the catalyst window is finally close. That does not make it safe. It makes it interesting.

My read is simple. ABCL is compelling below $4 if you understand that you are underwriting a clinical catalyst, not a proven business model. Between $4 and $5, it is still watchable but less obviously cheap. Above $6 before Phase 2 data, I would start getting much more careful unless the May 11 update materially de-risks the story.

If you want boring, profitable, and screen-cheap, this is not your stock. If you want a cash-backed biotech with a live catalyst and enough short interest to matter if the data hit, ABCL deserves a spot on the watchlist.

This article is for informational purposes only and does not constitute financial advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

Sources: AbCellera company announcements on 2025 results and ABCL635 clinical timing; Stock Analysis valuation and balance sheet data; ClinicalTrials.gov program details.