NEOG stock analysis thesis: Neogen is finally showing signs of operational stabilization, but the stock is no longer a deep-value recovery trade. After Q3 FY2026, management raised full-year revenue guidance to $857M-$860M, adjusted EBITDA stayed guided around $175M, and Food Safety continued to grow. The problem is valuation versus execution risk. At roughly 31x forward earnings with supplier issues still hitting Animal Safety, this is a quality turnaround story, not a no-brainer bargain.

If you want one line: Neogen is investable on pullbacks, but the margin for error is tighter than the headline guidance raise suggests.

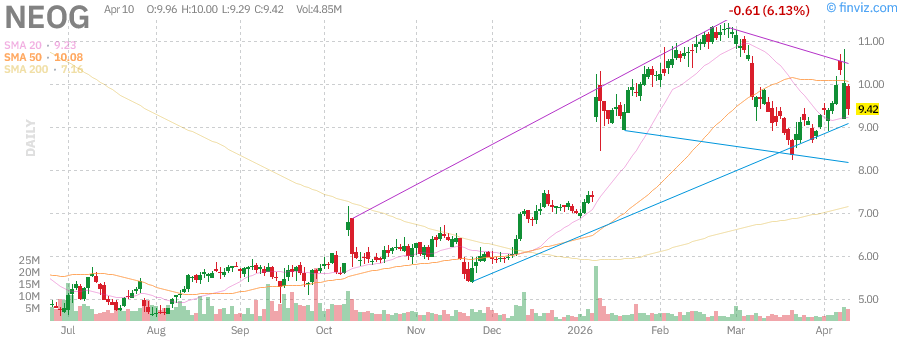

Why NEOG Is Back on the Radar in 2026

Neogen’s April 9 Q3 FY2026 update gave investors a mixed but improving setup:

- Q3 revenue: $211.2M (down 4.4% year over year)

- Core growth: +0.1%

- Food Safety revenue: $156.7M (up 2.6%; core +4.0%)

- Animal Safety revenue: $54.5M (down 20.1%; core -8.7%)

- Q3 adjusted EBITDA: $48.2M with 22.8% margin

- Q3 free cash flow: $11.1M

- FY2026 revenue guide raised to $857M-$860M from $845M-$855M

- FY2026 adjusted EBITDA guide maintained at ~$175M

The market liked the guidance raise, but it did not ignore the quality of the quarter. Animal Safety was weak, and management directly blamed third-party supplier disruptions. That means investors are still underwriting operational repair, not just demand recovery.

Key Metrics Investors Should Watch

Using current market data, NEOG screens as a mid-risk small-cap turnaround:

- Market cap: ~$2.05B

- Sales (TTM): ~$870.5M

- Forward P/E: ~31.1x

- Short interest: ~10.07M shares (short float ~4.66%)

- Analyst target (consensus snapshot): ~$11.62

- Share count: ~217.7M outstanding

That is not distressed pricing. The stock is being valued as a company that can execute a clean margin rebuild from here.

Bull Case for Neogen

1) Food Safety is acting like the core growth engine it was supposed to be.

Food Safety posted +2.6% reported growth and +4.0% core growth in Q3. Within that segment, indicator testing and culture media grew 11.0%, and bacterial/general sanitation grew 5.5%. That mix matters, because investors want recurring, compliance-driven demand in food quality workflows.

2) EBITDA margin discipline is improving.

Adjusted EBITDA margin was 22.8% in Q3, up sequentially by 110 basis points. That suggests management is finding real operating leverage through cost controls, even while one segment is under pressure.

3) Cash generation is positive and guidance credibility improved.

Q3 operating cash flow of $22.7M and free cash flow of $11.1M are not spectacular, but they are directionally right for a turnaround. Management also raised revenue guidance while holding EBITDA targets, which is usually better than a cosmetic raise with hidden dilution in profitability.

4) Genomics divestiture can de-risk the balance sheet.

Neogen agreed to sell its Genomics business to Zoetis for $160M, with expected net proceeds around $140M. If executed cleanly, that capital can support deleveraging and reduce financial risk at a time when investors are punishing over-levered small caps.

Bear Case for Neogen

1) Animal Safety weakness is not theoretical, it is in the numbers.

Animal Safety revenue dropped 20.1% year over year in Q3, with core growth down 8.7%. Management called out supplier disruptions, but investors do not get paid for explanations, they get paid for repaired execution. Until that segment normalizes, the recovery narrative stays fragile.

2) Gross margin pressure has not disappeared.

Q3 gross margin was 46.9% versus 49.9% a year ago. Management cited Petrifilm transition costs, tariff effects, and inventory write-offs. Even if those are temporary, they are still real drags right now.

3) Valuation is not cheap relative to uncertainty.

A forward P/E near 31x is a premium multiple for a company still proving consistency. The market is already pricing in cleaner execution over the next few quarters. If improvements slip, rerating risk is real.

4) Turnarounds fail when “temporary” issues keep repeating.

Neogen has multiple moving parts: supply chain repair, manufacturing transition, portfolio reshaping, and margin normalization. Any one of those can slip. Investors should assume at least one does.

Catalysts to Watch Through the Next Two Quarters

- Animal Safety recovery evidence: Any quarter showing clear stabilization in this segment will likely matter more than headline revenue.

- Petrifilm transition progress: Management says transition remains on track for completion by November 2026. Hitting this timeline is a credibility test.

- Genomics divestiture close: Expected by Q2 FY2027. Clean execution and debt reduction messaging could support multiple stability.

- EBITDA conversion quality: Watch whether adjusted EBITDA strength begins to flow into sustained free cash flow.

How NEOG Compares to Other Margin of Alpha Setups

If you’ve been reading Margin of Alpha’s recent small-cap coverage, NEOG sits in a different bucket than pure deep-value names:

- Compared with DLX, NEOG has less obvious valuation support.

- Compared with RELY, NEOG has a more complicated operational repair story.

- Compared with PAHC, NEOG has a stronger transformation narrative but similar execution sensitivity.

That means position sizing matters. NEOG is not a “set it and forget it” small cap. It is a monitoring-heavy name where quarter-to-quarter evidence can change the thesis quickly.

Verdict: Buy, Hold, or Avoid?

Verdict: Hold / selective buy on weakness.

Neogen is doing enough right to stay on the watchlist and potentially in a portfolio, especially for investors looking for a food safety plus animal health turnaround with identifiable catalysts. But at current valuation, you are paying for recovery before all the recovery work is done.

I would be more aggressive if either of these happens:

- Animal Safety stabilizes with at least flat-to-positive core growth, or

- The stock reprices lower and gives a wider margin of safety.

Until then, this is a quality turnaround that deserves respect, not blind conviction.

Sources and Data Checks

- Neogen Q3 FY2026 results and FY2026 guidance update (Business Wire release, April 9, 2026)

- Stock metrics snapshot (Finviz quote data for NEOG)

- Related company action: Genomics business sale to Zoetis announcement

This is not financial advice. Do your own research.