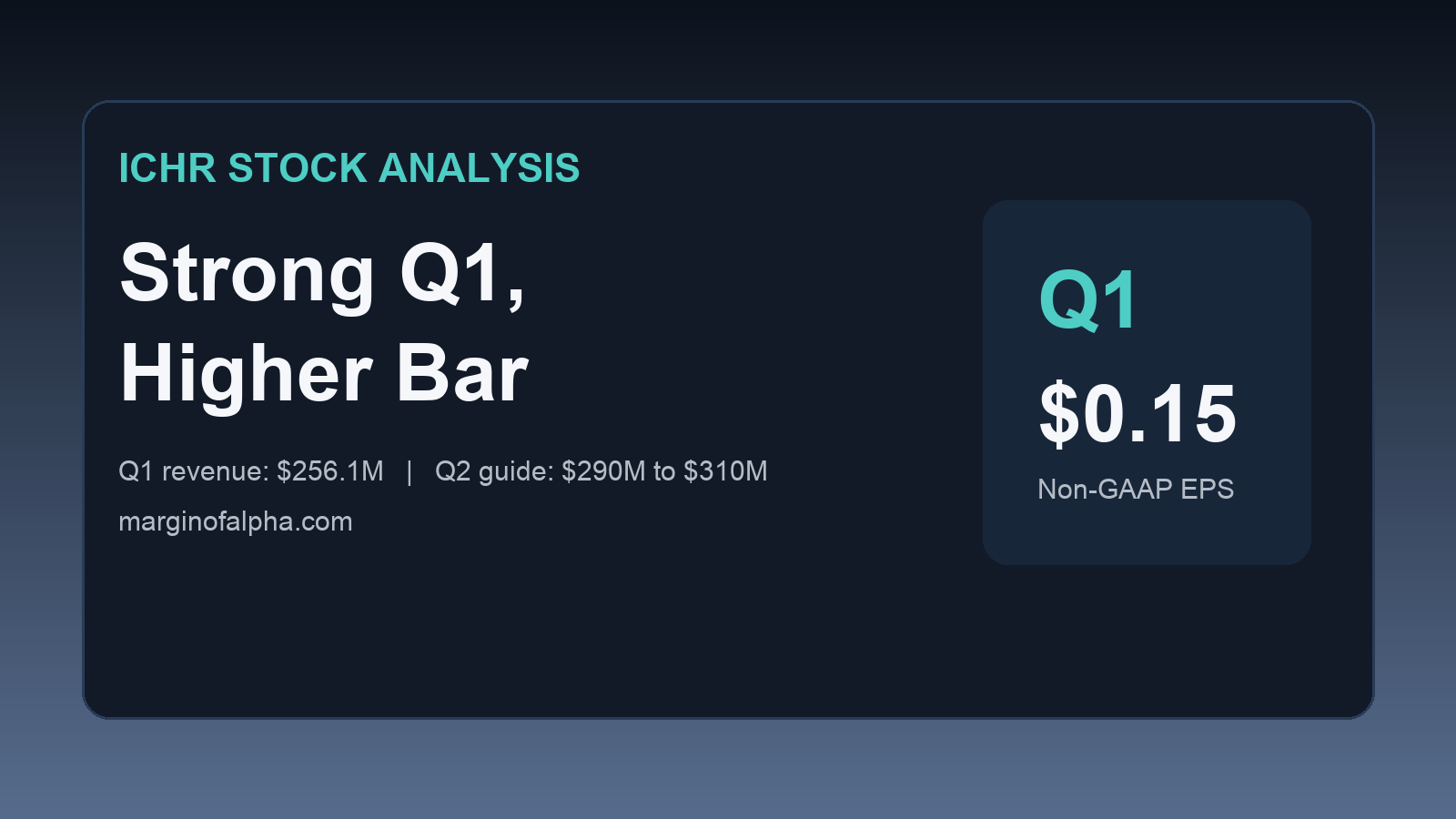

Ichor Holdings just gave the bull case fresh evidence. Q1 2026 revenue came in at $256.1 million, ahead of the midpoint of guidance, non-GAAP EPS hit $0.15, and Q2 guidance points to another step up to $290 million to $310 million. That matters because ICHR stock analysis is no longer about whether the cycle is turning. It is about whether the stock already priced in most of the good news.

My read: Ichor looks stronger than it did in February, but not cheap enough to chase blindly after the recent run. If you want semiconductor equipment exposure tied to U.S. fab buildouts and gate-all-around process complexity, ICHR is a legitimate name. If you are buying after the move, you need a clear view on margins and customer concentration, not just a generic “AI chips need more equipment” story.

Why ICHR stock analysis looks better after Q1

Ichor builds the gas and chemical delivery subsystems that sit inside semiconductor capital equipment. It is a picks-and-shovels business for wafer fabrication. Lam Research and Applied Materials need these systems to run etch and deposition tools, and those tool categories should benefit as advanced nodes, high-bandwidth memory, and gate-all-around architectures push process complexity higher.

The new quarter backed that story up with real numbers. According to the company's first-quarter 2026 earnings release, revenue was $256.1 million, up from $223.6 million in Q4 2025 and $244.5 million in Q1 2025. GAAP gross margin improved to 12.6% from 9.4% last quarter. Non-GAAP gross margin improved to 12.8% from 11.7%. Non-GAAP net income was $5.3 million, or $0.15 per diluted share, versus essentially breakeven last quarter.

That is not a hype quarter. That is a real operational improvement quarter.

The setup changed from “prove it” to “can they hold it”

The old Ichor debate was straightforward. The company had to prove that Q4 2025 was actually the trough, that Malaysia capacity would help margins, and that semiconductor equipment demand would not roll over again. Q1 made that case a lot easier to believe.

Management now expects Q2 revenue between $290 million and $310 million, with GAAP EPS of $0.10 to $0.20 and non-GAAP EPS of $0.25 to $0.35. At the midpoint, that implies roughly 17% sequential revenue growth from Q1. For a company that reported $947.7 million of full-year 2025 revenue, that points toward a very different exit rate by the end of 2026 if execution holds.

This is exactly why the paper portfolio added ICHR on May 28. It gives marginofalpha exposure to semiconductor infrastructure instead of another biotech or software name, and it ties into a real macro tailwind, domestic fab capex and the broad semiconductor equipment cycle. The portfolio entry uses an entry price of $73.74, a target of $96, and a stop at $61.

The bull case: more wafer-fab spend, more process complexity, more Ichor content

The cleanest bull case here is not hard to understand.

First, wafer fabrication equipment demand appears to be strengthening again. Management said the company saw a stronger demand environment and accelerated customer delivery timelines. That lines up with the broader reshoring and domestic chip-capex story that has been building since the CHIPS Act spending wave started feeding through supplier stacks.

Second, Ichor is exposed to the right layers of complexity. As advanced-node manufacturing shifts deeper into gate-all-around and high-bandwidth-memory-linked production ramps, etch and deposition steps matter more. Ichor's fluid delivery systems sit right in that workflow. More process intensity per wafer can mean more subsystem demand even before you talk about new fabs.

Third, the margin story is finally moving in the right direction. GAAP operating margin turned positive at 0.8% in Q1 2026 after being -6.2% in Q4 2025. Non-GAAP operating margin improved to 3.4% from 1.2%. If the Malaysia buildout and internalization strategy keep lifting margins through the year, earnings can grow faster than revenue.

That last point matters most. Semiconductor suppliers can look cheap or expensive depending on where you catch them in the margin cycle. If Ichor is still early in a margin recovery, the stock can justify a higher multiple than skeptics expect.

The bear case: the stock may already know all of this

Here is the part bulls do not get to ignore. Margin improvement stories are great. Chasing them after the market already started pricing them in is where people get hurt.

Ichor already has an older marginofalpha article from February because the stock had made a huge move even then. Since that earlier piece, the company did what it needed to do operationally. The problem is that better operations do not automatically equal a better entry price.

The main bear points are still pretty clear:

- Customer concentration remains real. Ichor depends heavily on a small number of semiconductor equipment OEMs. If Lam Research or Applied Materials slow orders, Ichor feels it quickly.

- Cash dipped in Q1. Cash and cash equivalents fell to $89.1 million from $98.3 million at year-end 2025, while accounts receivable and inventory both rose. That is not a crisis, but it shows growth is still consuming working capital.

- GAAP profitability is only just turning. Q1 GAAP EPS was still -$0.07. This is improving, but it is not the same thing as a mature, consistently profitable compounder.

- The balance sheet is fine, not pristine. Total current debt was $6.25 million and long-term debt still sits on the books. In a healthy demand environment that is manageable. In a downcycle it matters more.

- The stock is not an underfollowed secret anymore. Once a semiconductor infrastructure name becomes an obvious reshoring winner, the easy multiple expansion is usually gone.

The simplest way to say it: the business improved, but the market may have front-run part of the improvement.

What I would watch next

For this ICHR stock analysis to stay bullish, I want three things in the next quarter or two.

1. Q2 has to land near the high end of guidance. Management guided to $290 million to $310 million in revenue. If that comes in soft after such a strong Q1 and such a confident setup, the stock probably gets punished.

2. Gross margins need to keep climbing. Q1 GAAP gross margin of 12.6% is better, but not amazing. If that number stalls, the earnings leverage story weakens fast.

3. Working capital needs to look cleaner. Receivables rose to $93.1 million and inventory rose to $252.3 million. Some of that is normal in a ramp. Too much of it can become a warning sign if customer timing slips.

If those three things happen, the case for a higher target gets easier. If one or two break the wrong way, the stock can still be a fine company and a mediocre trade.

How it compares with other marginofalpha names

ICHR is a different animal than some recent portfolio and site names. HYLN stock analysis is a much earlier commercialization bet. EVER stock analysis is more of a recovering internet platform story. CPRX stock analysis is about cash-rich pharma execution and capital allocation.

Ichor sits in the middle. It has more real revenue than the speculative names, but it is still cyclical enough that entry price matters a lot. That makes it interesting for investors who want small-cap exposure with actual industrial substance behind it.

Verdict: strong quarter, tougher stock

Ichor earned a better article than the one it needed in February. Q1 2026 showed real revenue acceleration, better margins, and a Q2 guide that says the upcycle is still building. That is the good news.

The harder part is valuation discipline. I do not think the right takeaway is “buy any dipless semiconductor supplier because fabs are coming back.” The right takeaway is narrower: ICHR is a legitimate semiconductor infrastructure name with improving execution, but the stock now needs continued margin expansion and clean follow-through to justify aggressive upside targets.

If I already owned it from lower levels, I would be comfortable holding as long as Q2 confirms the ramp. If I were opening a fresh position, I would want a better entry than an emotionally-chased breakout. The paper portfolio target of $96 is possible if the cycle stays hot and margins keep climbing, but the stock has to earn that path quarter by quarter.

Bottom line: Ichor looks stronger operationally than it did three months ago. That makes it investable. It does not automatically make it cheap.

This article is for informational purposes only and does not constitute financial advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.